How To Reset Your Money Life When You Feel Behind

You can be smart, accomplished, and still feel behind with money.

Maybe your income looks good on paper, but your savings balance makes you cringe. Maybe you are carrying debt that feels heavy and secret. Or you are earning more than ever and still wondering, “Where is it all going?”

This is not a personal failure. It is a signal. A quiet nudge that your money life needs a reset, not a complete teardown.

Below is a simple, non-judgmental framework to help you move from vague anxiety to clear next steps.

Step 1: Pause the shame spiral

Before any spreadsheet, there is your nervous system. When you feel behind, your brain wants to jump to extremes: “I’ll never catch up,” or “I have to fix everything this month.”

That urgency often leads to avoidance or impulsive decisions. Neither helps.

Try this instead:

- Name what is actually true today – not the story about it. For example: “I have $8,000 in credit card debt and $2,500 in savings.” That is data, not a verdict.

- Separate your identity from your numbers – your net worth is not your self-worth. You are a whole person who has money patterns, not a “mess.”

- Decide this is a reset season – not punishment, not emergency, just a focused season of getting current with your money.

From this calmer place, you can actually see what needs to change.

Step 2: Get a clear, simple snapshot

You do not need a perfect budget to start. You need a snapshot that fits on one page.

Gather:

- Income – your take-home pay per month (after taxes and benefits). If it varies, use a conservative average.

- Fixed essentials – rent or mortgage, utilities, groceries, transportation, insurance, childcare, minimum debt payments.

- Debts – balances, interest rates, and minimum payments for each card or loan.

- Cash and savings – checking, savings, emergency fund, any short-term sinking funds.

Write it out in a simple list or basic spreadsheet. No categories beyond what you will actually use.

The goal is not precision; it is visibility. Once you can see the whole picture, your brain has something concrete to work with instead of a vague sense of dread.

Step 3: Define what “not behind” looks like for you

Feeling behind is relative. Compared to what? Social media? A colleague? An imaginary version of yourself?

To reset, you need your own definition of “on track.” Consider these anchors:

- Stability – bills paid on time, a small emergency buffer, debt under control.

- Flexibility – room for travel, experiences, or time off without panic.

- Future you – retirement and long-term goals getting consistent, if modest, contributions.

Then translate that into 2–3 concrete targets for the next 12–18 months, such as:

- “Build a $5,000 emergency fund.”

- “Pay off my highest-interest credit card.”

- “Start investing 10% of my income for retirement.”

Now you are not chasing a vague idea of “catching up.” You are moving toward specific milestones that matter to you.

Step 4: Create a calm, realistic cash flow plan

Instead of a strict budget you will abandon in two weeks, build a cash flow plan that reflects your real life.

Start with your monthly take-home income. Then:

- Cover essentials first – housing, food, utilities, transportation, insurance, minimum debt payments.

- Set a starter emergency fund target – if you have less than one month of expenses saved, aim for $1,000–$2,000 as a first milestone, then build toward 3–6 months over time.

- Choose one primary focus – either building savings or paying down high-interest debt. You can do both, but one gets priority for extra dollars.

- Give your fun spending a clear container – instead of “stop eating out,” decide: “I have $X per month for restaurants and drinks, guilt-free.”

Run the numbers. If they do not work on paper, that is information, not failure. It means something has to shift: income, expenses, or timeline.

Ask yourself:

- “What can I reduce or pause for the next 3–6 months without feeling deprived, just intentional?”

- “Where is there low-hanging fruit: subscriptions, fees, unused services?”

- “Is there a realistic way to increase income temporarily: consulting, a raise conversation, a small side project?”

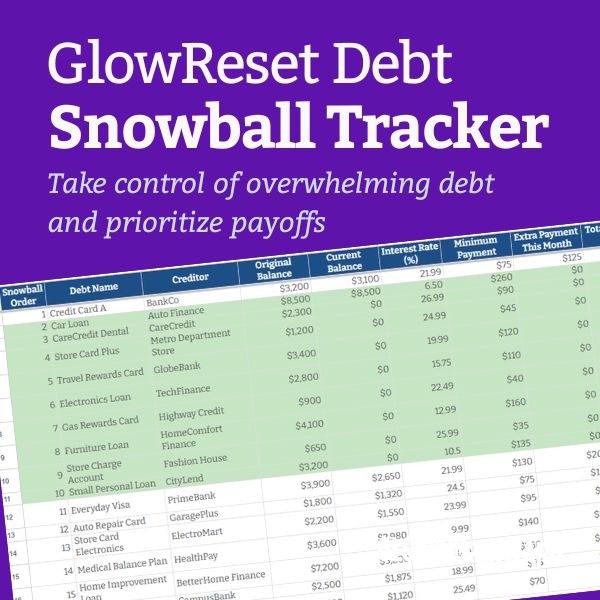

Step 5: Tackle debt with a clear strategy

Debt often carries the most emotional weight. Instead of avoiding statements, choose a simple plan.

Two common approaches:

- Debt avalanche – pay extra toward the highest-interest rate first while making minimums on the rest. This saves the most money over time.

- Debt snowball – pay extra toward the smallest balance first for faster emotional wins, then roll that payment into the next debt.

Pick the method that you are most likely to stick with, not the one that looks best on paper.

Then decide:

- How much extra you can realistically send to debt each month.

- Which card or loan is your current “target.”

- What you will do when you pay one off (for example, split the freed-up payment between the next debt and savings).

Put this plan in writing. Seeing it laid out turns a heavy cloud of “I have so much debt” into a series of steps you are already taking.

Step 6: Automate what you can

Willpower is not a financial strategy. Automation is.

Once you know your priorities:

- Automate minimum payments on all debts to avoid late fees and stress.

- Set up automatic transfers to savings on payday, even if it is a small amount. Saving $50 consistently beats saving $500 once.

- Automate retirement contributions through your employer plan or an individual account.

Automation moves your money toward your goals before you can talk yourself out of it. You can always adjust the amounts as your situation changes.

Step 7: Build simple money rituals

To stay out of overwhelm, you need a gentle rhythm, not constant monitoring.

Try two basic rituals:

- Weekly 15-minute money check-in

- Log into your accounts.

- Note balances, upcoming bills, and any unusual spending.

- Decide one small action: move $20 to savings, cancel a subscription, or schedule a debt payment.

- Monthly reset

- Review what came in and what went out.

- Celebrate progress, even if it is small: “I paid every bill on time,” or “I added $100 to savings.”

- Adjust next month’s plan based on what is actually happening, not what you wish would happen.

These rituals keep you in relationship with your money without letting it take over your mental space.

Step 8: Give yourself a longer timeline

One reason you may feel behind is that you are expecting a one-year turnaround for a ten-year situation.

Instead, zoom out:

- What would “solid and steady” look like in three years?

- What if you gave yourself five years to fully reset, instead of demanding perfection in twelve months?

Longer timelines create room for life to happen: job changes, caregiving, health, relationships. You are allowed to adjust your plan as your reality shifts.

Progress is not linear. Some months you will move faster, some months you will simply hold the line. Both count.

Step 9: Allow support

You do not have to do this alone or know everything yourself.

Support can look like:

- A trusted friend you check in with about money goals.

- A therapist or coach to help untangle emotional patterns around spending, scarcity, or over-responsibility.

- A fee-only financial planner to help you map out retirement, investing, and big-picture strategy.

Needing help is not a sign you are behind. It is a sign you are taking your financial life seriously.

You are not late to your own life

Feeling behind with money is painful, but it is also a powerful turning point. You can use that discomfort as information, not as a verdict.

Your reset does not have to be dramatic. It can be a series of calm, clear decisions: seeing your numbers, choosing your priorities, automating what you can, and giving yourself time.

You are not starting from zero. You are starting from experience. And that is a very strong place to begin.