How to Quiet Money Anxiety and Build a Calm, Confident Plan

If you’re successful on paper but still feel behind with money, you are not alone. Many high-achieving women quietly carry money anxiety: the sense that everyone else has it figured out, that you’re late to the game, or that one wrong move could undo everything.

This isn’t about intelligence or discipline. It’s about clarity, systems, and nervous-system safety. When money feels confusing or chaotic, your brain goes into protection mode: avoidance, overthinking, or impulsive decisions. The goal is not perfection. The goal is calm, informed choices.

Step 1: Separate your worth from your net worth

Before any spreadsheet or app, you need one core boundary: your value as a human is not tied to your bank balance, debt, or savings rate. When those get fused, every money task feels emotionally loaded and exhausting.

Try this simple mental shift:

- Data, not drama: Your numbers are information, not a verdict. They tell you where you are, not who you are.

- Progress, not perfection: You’re building a system that supports your life, not auditioning for “most responsible adult.”

- Season, not lifetime: Your current money reality reflects this season of life, not your permanent future.

When you feel shame or panic rising, pause and remind yourself: “These are just numbers. I’m allowed to learn.”

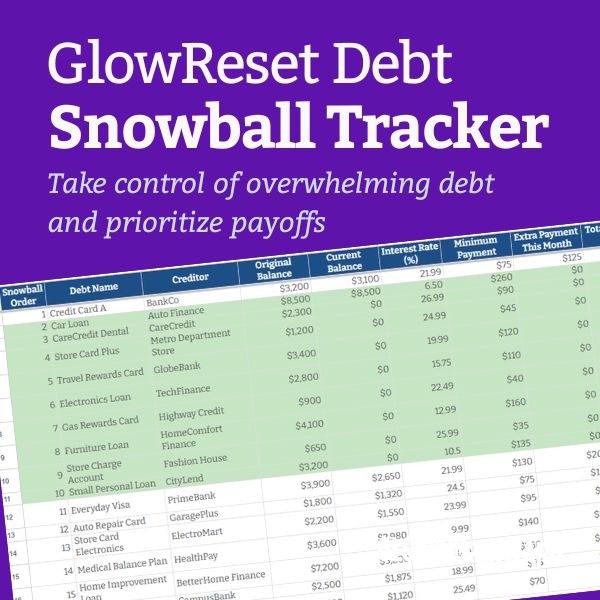

Step 2: Create a 20-minute money snapshot

Money anxiety thrives in vagueness. You might think, “I’m so behind,” but not be able to clearly say, “Here’s what’s coming in, going out, and what I actually own and owe.” The antidote is a quick snapshot, not a perfect master plan.

Set a 20-minute timer and capture four basics:

- 1. Income: List your after-tax monthly income from salary, business, bonuses (average them), and any other sources.

- 2. Fixed expenses: Housing, utilities, insurance, childcare, minimum debt payments, subscriptions.

- 3. Variable spending: Groceries, dining out, shopping, travel, wellness, etc. Use your last 1–3 bank or card statements for a rough average.

- 4. Debts and savings: Balances and interest rates for credit cards, loans, and your current savings/investment accounts.

It will not be perfect. That’s fine. The goal is to move from “I have no idea” to “I have a working picture.” You can refine later.

Step 3: Build a calm, realistic spending plan

Instead of a restrictive budget, think of a spending plan as a permission slip: you’re deciding in advance where your money will go so you don’t have to think about it every day.

Start with three simple buckets:

- Essentials (Needs): Housing, food, transportation, healthcare, minimum debt payments, basic childcare.

- Intentional Joy (Wants): Dining out, travel, beauty, clothes, hobbies, gifts, upgrades that genuinely matter to you.

- Future You (Goals): Emergency fund, investing, extra debt payments, big future purchases.

Look at your snapshot and assign rough amounts to each bucket. If everything feels tight, adjust in this order:

- First, see if any fixed expenses can be reduced or renegotiated over time (rent, insurance, subscriptions).

- Next, gently trim wants that don’t truly bring joy (the “meh” spending).

- Then, choose one or two priority goals for Future You instead of trying to fund everything at once.

A plan you can actually follow calmly beats an “ideal” plan you abandon in two weeks.

Step 4: Choose one priority for the next 90 days

Trying to fix everything at once is a fast track to burnout. Instead, choose one main money focus for the next 90 days. Examples:

- Build a starter emergency cushion of $1,000–$2,000.

- Pay off one high-interest credit card.

- Start (or restart) investing in a retirement account.

- Get three months of expenses clearly tracked and categorized.

Once you choose your focus, define a small, specific target. For example:

- “Transfer $150 every Friday into my emergency fund.”

- “Pay an extra $200 per month to Card A until it’s gone.”

- “Set up automatic 8% of my paycheck into my 401(k).”

Specific and scheduled is kinder to your brain than vague intentions like “save more” or “spend less.”

Step 5: Automate so you don’t have to rely on willpower

Automation is one of the most powerful tools for women who are already mentally overloaded. You do not need more decisions in your day. You need fewer.

Consider automating:

- Bills: Set up auto-pay for fixed bills and minimum debt payments to avoid late fees and mental clutter.

- Savings: Schedule automatic transfers to your emergency fund or other savings right after payday.

- Investing: Automate contributions to retirement accounts or investment accounts monthly or per paycheck.

Start small if you’re nervous. You can always adjust the amounts after a month or two. The point is to make your “good” money behavior the default, not the exception.

Step 6: Create a 30-minute monthly money date

Instead of constantly worrying about money in the background, give it a specific, limited place in your calendar. A monthly money date helps you feel in charge without obsessing.

Once a month, for 30 minutes, do this:

- Check balances in your accounts and debts.

- Look at the last month’s spending by category.

- Celebrate one win (no matter how small).

- Choose one tiny adjustment for the coming month.

Make it as pleasant as possible: favorite drink, music, a candle. This may sound small, but pairing money tasks with comfort helps your nervous system stay regulated, so you can think clearly instead of spiraling.

Step 7: Address emotional triggers around money

Money is rarely just math. It’s family stories, cultural expectations, and past experiences. If you notice strong reactions—panic when you open your banking app, guilt when you spend on yourself, or dread around bills—that’s not a personal flaw. It’s a signal.

Try this simple practice when you feel triggered:

- Pause and take three slow breaths.

- Name what you’re feeling: “I feel anxious,” “I feel ashamed,” “I feel confused.”

- Ask: “What story am I telling myself right now?” (For example: “I’ll never catch up,” “I’m bad with money,” “It’s too late.”)

- Gently challenge the story: “Is this a fact, or a fear?” “What would I say to a friend who felt this way?”

Over time, this helps you respond to money with curiosity instead of self-criticism. That shift alone can change the choices you make.

Step 8: Redefine what “being good with money” means for you

It’s easy to measure yourself against someone else’s version of financial success: owning a home by a certain age, hitting a specific net worth, or following a rigid investing strategy. But your life, responsibilities, and values are unique.

Consider your own definition of “financially well.” It might include:

- Feeling calm when you check your accounts.

- Having a buffer so one unexpected bill doesn’t derail everything.

- Spending on what genuinely matters to you without constant guilt.

- Knowing you’re moving, even slowly, toward long-term security.

When you define success on your terms, you can make aligned decisions instead of chasing someone else’s timeline.

Step 9: Allow yourself to be a beginner, even if you’re successful elsewhere

High-achieving women often feel they “should” already know all of this. That belief keeps many from asking questions, hiring help, or starting at all. You’re allowed to be a beginner with money, even if you’re advanced in your career or life.

Being new at something doesn’t mean you’re behind. It means you’re learning. Every step you take—opening the app, writing down your numbers, setting up one automatic transfer—is evidence that you’re building a different future.

Your finances don’t have to be perfect to be powerful. They just need your attention, a bit of structure, and a lot of self-compassion.

You are not late. You are right on time to start now.