Money Reset: A Calm, Clear Way to Get Back On Track

If you’re successful on paper but quietly stressed about money, you’re not alone. Many high-achieving women feel behind, overwhelmed, or like they “should” be further along financially.

This isn’t about blame or perfection. It’s about a reset: a calm, clear way to see where you are, decide what you want, and take simple steps forward.

Step 1: Pause the shame spiral

Before any numbers, you need one thing: a clean mental slate.

Feeling behind, embarrassed, or “bad with money” makes it harder to take action. Your brain will want to avoid anything that feels like proof you’re failing.

Instead, try this reframe:

- Money is a skill, not a personality trait. You weren’t born knowing how to manage taxes, investments, or debt. Skills can be learned at any age.

- Your past decisions made sense with what you knew then. You had different priorities, information, and pressures. That context matters.

- You can improve your finances without fixing your entire life first. You don’t need the perfect job, partner, or schedule to start.

Your only job in this step: decide that looking at your money is an act of self-respect, not self-criticism.

Step 2: Get the real picture (without spreadsheets drama)

Clarity is more calming than guessing. You don’t need a complicated system. You just need a snapshot of where things stand today.

Block 30–60 minutes. Grab a notebook or notes app. Log in to your accounts and write down:

- Cash: checking, savings, cash apps

- Debt: credit cards, student loans, personal loans, car loans, lines of credit

- Investments: 401(k), 403(b), IRA, brokerage, HSAs

- Recurring bills: rent/mortgage, utilities, subscriptions, insurance, childcare, loans

Don’t try to fix anything yet. Just gather.

If you feel anxious while doing this, pause and remind yourself: “Information is power. I’m just collecting data.”

When you’re done, circle three numbers:

- Total cash

- Total debt

- Total invested

These three numbers are your starting line. Not your worth. Not your future. Just your current snapshot.

Step 3: Define what “on track” actually means for you

Many women feel behind because they’re measuring themselves against a vague, invisible standard: some mix of social media, friends, and what they think “should” be true by this age.

Instead, define your own version of “on track.” Ask yourself:

- Short term (next 12 months): What would make me feel more stable and less stressed?

- Medium term (3–5 years): What do I want my life to look like, and what money would support that?

- Long term (10+ years): What kind of freedom or options do I want?

Examples of clear, grounded goals:

- “Have three months of expenses in savings so I don’t panic every time something breaks.”

- “Pay off my highest-interest credit card so I stop feeling like I’m treading water.”

- “Consistently invest a set amount each month for future me.”

Pick one main focus for the next 6–12 months. Not five. One. That focus will guide your decisions.

Step 4: Build a simple, realistic money flow

Instead of a strict budget you’ll abandon in two weeks, create a simple money flow: a plan for where your money goes when it comes in.

Start with your monthly take-home pay. Then assign it in this order:

- 1. Essentials: housing, utilities, groceries, transportation, minimum debt payments, childcare, basic insurance

- 2. Safety: emergency savings or a small buffer account

- 3. Priority goal: the one focus you chose (debt, savings, or investing)

- 4. Joy and lifestyle: dining out, travel, beauty, shopping, hobbies

Two key ideas:

- Automate what you can. Set automatic transfers for savings, debt payments, and investing right after payday. This reduces decision fatigue and helps you follow through on your plan.

- Give yourself a realistic “fun” number. Cutting everything enjoyable usually backfires. Choose an amount you can spend freely without guilt.

If the numbers don’t work (for example, essentials already eat most of your income), that’s data, not failure. It just means your next step may be income-focused (negotiating pay, side income, or reducing big fixed costs) rather than obsessing over small expenses.

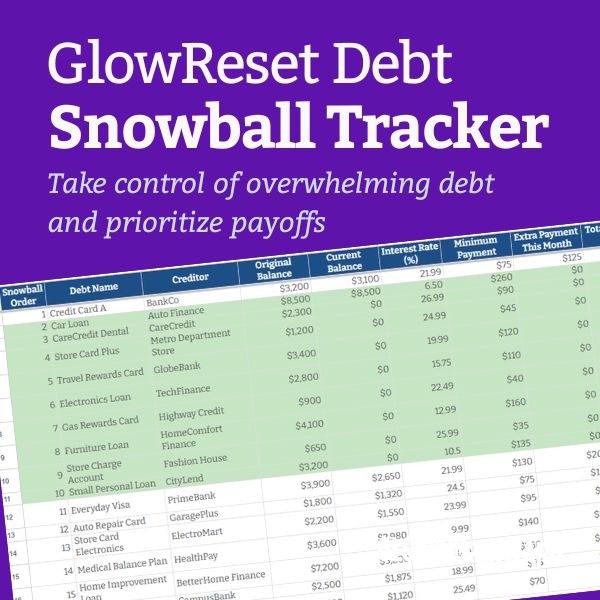

Step 5: Create a calm debt and savings strategy

If you have debt, especially high-interest debt, it can feel like a heavy cloud over everything. You don’t need to erase it overnight. You just need a clear plan.

List each debt with:

- Balance

- Interest rate

- Minimum payment

Then choose one approach:

- Highest interest first (debt avalanche): Mathematically smartest. You pay extra toward the highest interest rate while paying minimums on the rest.

- Smallest balance first (debt snowball): Emotionally satisfying. You pay extra toward the smallest balance to get quick wins.

There’s no morally superior choice. Pick the one you’re more likely to stick with.

For savings, start with a small, reachable target. For example:

- First goal: $500–$1,000 as a starter emergency fund

- Next: one month of expenses

- Then: three months of expenses

Keep this in a separate savings account so it doesn’t blend into your checking balance. Label it something supportive like “Peace of Mind Fund” instead of “Emergency.” Language matters.

Step 6: Support future you with simple investing

If you feel behind on retirement or investing, it’s easy to freeze and do nothing. But even small, consistent amounts can make a real difference over time.

Start with what’s available to you:

- Work retirement plan: 401(k), 403(b), or similar. If your employer offers a match, aim to contribute at least enough to get the full match. That’s part of your compensation.

- Individual accounts: If you don’t have a work plan, or you want to do more, look into an IRA or a simple brokerage account.

You don’t need to become a stock expert. Many women do well starting with:

- A low-cost target-date retirement fund, or

- A low-cost broad index fund (like a total market or S&P 500 fund)

The key is consistency. Even $100–$200 a month, invested over years, can change your future options.

Step 7: Make money care a regular ritual

Money feels less overwhelming when it becomes a routine, not an emergency project.

Try a weekly 20–30 minute “money check-in.” Keep it as neutral and gentle as possible:

- Log in to accounts and glance at balances

- Confirm bills and automatic transfers are scheduled

- Note any upcoming expenses (trips, renewals, gifts)

- Decide one small action for the week (cancel a subscription, move $50 to savings, increase a payment by $20)

Pair it with something pleasant: a candle, music, a favorite drink. Train your brain to associate money time with calm, not panic.

Step 8: Redefine what being “good with money” looks like

Being good with money is not about never making mistakes, never using credit, or hitting some magic net worth number by a certain age.

It looks more like this:

- You know your numbers and check in regularly.

- You have a simple plan that reflects your real life and values.

- You adjust when life changes instead of avoiding your accounts.

- You treat yourself with respect, even when you’re learning or course-correcting.

You’re not behind. You’re right on time to start your next chapter with money. One clear step, one calm decision, one small action at a time.