Money Overwhelm: How to Get Calm, Clear, and Back in Control

If you’re successful on paper but secretly stressed about money, you are not alone.

Maybe you make a solid income, yet your savings feel thin. Maybe you’re carrying quiet debt, or you’re not sure where your money actually goes each month. You might feel like you “should” be further ahead by now, and that thought alone is exhausting.

This isn’t about blaming past choices. It’s about building a calmer, clearer relationship with your money from today forward.

Step 1: Shift from shame to data

Money overwhelm usually comes from a swirl of feelings, not facts. The fastest way to feel more grounded is to move from “I’m bad with money” to “I’m looking at information.”

For the next week, your only job is to gather data, not fix anything.

- List your accounts: checking, savings, credit cards, loans, retirement, investment apps.

- Write down balances: what you have and what you owe, without judgment words like “only” or “too much.”

- Capture your monthly numbers: income after tax, rent or mortgage, utilities, groceries, transportation, childcare, subscriptions, debt payments, and anything else that’s recurring.

If this feels intense, break it into 15-minute blocks. One card here, one account there. You are simply collecting facts, the way you would for a work project.

When you notice self-criticism, try a neutral reframe: “Interesting. Now I know.” That’s it. Awareness is progress.

Step 2: Define what “enough” looks like for you

It’s hard to feel financially secure when the goal is vague. “Be better with money” is not a target. “Have more” is not a target. You need a personal definition of “enough” that fits your life, not someone else’s.

Start with three simple numbers:

- Stability: 1–3 months of essential expenses in cash (rent, food, utilities, transportation, minimum debt payments).

- Security: 3–6 months of those same essentials.

- Freedom: money for goals that matter to you: travel, career changes, time off, starting a business, or simply breathing room.

Use your actual monthly essentials from Step 1. If your essentials are $4,000/month, then:

- Stability target: $4,000–$12,000

- Security target: $12,000–$24,000

These are not pass/fail numbers. They are reference points so you can say, “I’m at 0.5 months now; I’m moving toward 1 month,” instead of “I’m so behind.”

Step 3: Create a calm, simple money flow

Once you know your numbers, you can design a money system that runs with less emotional effort. Think of it as a calm flow instead of a strict budget.

Use a simple structure:

- Account 1: Bills & basics. Your paycheck lands here. All fixed bills and essentials are paid from this account.

- Account 2: Freedom fund (savings). Automatic transfers move money here every time you’re paid, even if it’s a small amount.

- Account 3: Fun & flexible. This is for dining out, shopping, and extras. When it’s empty, you’re done for the month—no spreadsheets required.

Then, decide on a basic percentage plan. For example:

- 60–70% to bills and essentials

- 10–20% to savings and debt payoff

- 10–20% to fun and lifestyle

The exact numbers are less important than consistency. Start with what’s realistic, not what’s ideal. If 5% to savings is all that fits right now, that still counts. You’re building a habit and a pathway, not chasing perfection.

Step 4: Tidy your spending, gently

Most women who feel behind with money are not reckless. They’re busy. Money leaks happen quietly: unused subscriptions, impulse buys when you’re tired, convenience spending because your schedule is packed.

Instead of a restrictive “no-spend” mindset, try a gentle tidy-up:

- Cancel the obvious: subscriptions or memberships you forgot about or don’t truly use.

- Cap the autopilot spending: set a monthly limit for things like rideshares, delivery apps, or online shopping.

- Choose your luxuries on purpose: decide what you genuinely love (maybe skincare, travel, or fitness) and allow room for it, while trimming the things you don’t care about as much.

This is about alignment, not restriction. Your money should reflect your real life and values, not a generic rulebook.

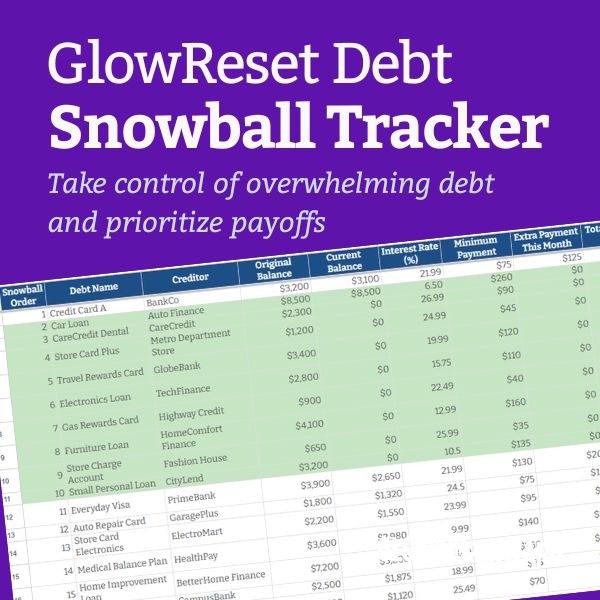

Step 5: Make a simple plan for debt

Debt can create constant background stress, even when you’re handling everything else well. The goal is to move from vague worry to a clear, manageable plan.

Start by listing each debt with:

- Balance

- Interest rate

- Minimum payment

Then choose one of two approaches:

- Highest interest first (avalanche): Mathematically efficient. You pay extra toward the debt with the highest rate while paying minimums on the rest.

- Smallest balance first (snowball): Emotionally motivating. You clear smaller debts quickly to build momentum.

Pick the method that you are most likely to stick with. There is no moral prize for choosing the “perfect” strategy. The win is having a plan you can follow without burning out.

Step 6: Put your future self on the calendar

Feeling behind often comes from a sense that time is slipping by and you’re not doing “enough” for the future. Instead of trying to solve everything at once, schedule small, recurring actions.

- Monthly money check-in (30–45 minutes): Look at your accounts, update your numbers, and notice what’s working and what feels off.

- Quarterly upgrade (60 minutes): One focused improvement: increase your savings transfer by a small amount, negotiate a bill, review your retirement contributions, or finally roll over an old 401(k).

- Annual vision session: Revisit your definition of stability, security, and freedom. What’s changed? What do you want your money to make possible in the next 1–3 years?

Put these on your calendar like any important meeting. You are building a relationship with your future self, one appointment at a time.

Step 7: Separate your worth from your net worth

Many high-achieving women quietly link their self-esteem to their financial status. If you’ve ever thought, “I should be further along by now,” you’ve felt this.

Here’s the truth: your net worth is a data point, not a verdict. It reflects a mix of factors—family background, career path, caregiving responsibilities, health, geography, and timing—not just discipline or intelligence.

When you notice comparison creeping in, try this reframing question: “Given my actual life, what does progress look like for me this year?”

Maybe it’s paying off one card. Maybe it’s building your first month of emergency savings. Maybe it’s finally understanding your investments instead of avoiding them.

Progress is personal. You are allowed to define it for yourself.

Step 8: Build a quiet support system

You do not have to do this alone. Support doesn’t have to mean broadcasting your situation to everyone. It can be discreet and tailored to your comfort level.

- Professional help: a fee-only financial planner, money coach, or accountant who explains things in plain language and respects your goals.

- One trusted friend: someone you can share wins and worries with, without performance or pretending.

- Learning in small doses: a podcast, book, or newsletter that teaches you one concept at a time—no scare tactics, no shaming.

Your financial life is part of your overall wellbeing, just like your health or relationships. Getting support is a sign of leadership in your own life, not a sign of failure.

Moving forward, not catching up

You might still wish you had started earlier. Most people do. But you are here now, paying attention. That matters more than you think.

Instead of trying to “catch up” to an invisible standard, focus on this question: “What is the next right step for me this month?”

Maybe it’s gathering your numbers. Maybe it’s opening a separate savings account. Maybe it’s scheduling that first money check-in on your calendar.

Your financial story is not fixed. It is being written in small, doable steps. You are allowed to start exactly where you are and move forward—calmly, clearly, and on your own terms.