Money Clarity When You Feel Behind: A Calm Reset for Your Finances

If you are successful on paper but feel behind with money, you are not alone. Many women who are thriving in their careers still feel anxious, disorganized, or unsure about their financial next steps.

This is not a character flaw. It is usually a mix of busy seasons, unclear systems, and money stories you absorbed over time. The good news: you do not need a perfect plan to move forward. You just need a clear, calm process.

This guide walks you through a simple reset you can do in a weekend or over a few evenings. No shame. No extreme budgeting. Just practical clarity.

Step 1: Define What “Enough” Looks Like For You

Before you open a single statement, decide what you are actually working toward. Without this, every number can feel wrong, small, or late.

Ask yourself:

- What does a comfortable life look like in the next 12 months? Think housing, food, fun, travel, wellness, and support (therapy, childcare, cleaning help).

- What do I want money to do for me in the next 3–5 years? Examples: pay off high-interest debt, build a 6-month emergency fund, change careers, start a business, take a sabbatical, support family.

- How do I want to feel about money? Calm, spacious, informed, supported, generous, secure.

Write down three sentences that start with “I want…” and one that starts with “I am willing…”

- I want to feel calm and clear about my money.

- I want my money to support rest, travel, and long-term security.

- I want to know exactly what is coming in and going out each month.

- I am willing to look at my numbers honestly and make a few changes.

This becomes your filter for every decision that follows.

Step 2: Create a Calm Money Snapshot

Instead of a full budget right away, start with a snapshot. The goal is awareness, not perfection.

Gather:

- Bank accounts

- Credit cards

- Loans (student, auto, personal, business)

- Retirement accounts (401(k), IRA, etc.)

- Investment accounts (brokerage, HSA, stock plans)

On one page or one simple spreadsheet, list:

- Cash: checking, savings

- Investments: retirement and non-retirement

- Debt: balance, interest rate, minimum payment

- Monthly income: after tax, average if it fluctuates

- Essential expenses: housing, utilities, food, transportation, minimum debt payments, childcare

Do not judge the numbers. You are collecting data, not grading yourself. If you feel activated, take a break, drink water, and come back. You are allowed to pace yourself.

Step 3: Separate Survival, Stability, and Growth

Once you see your snapshot, it is easier to decide what needs attention now and what can wait.

Think of your money in three layers:

- Survival: keeping the lights on and food in the fridge.

- Stability: building a buffer so emergencies do not derail you.

- Growth: investing for future you and bigger goals.

Start by estimating your monthly essentials:

- Housing (rent or mortgage, insurance, taxes if separate)

- Utilities and phone

- Groceries and basic household items

- Transportation

- Minimum debt payments

- Childcare or non-negotiable care expenses

Compare this to your average monthly income. If essentials are close to or above your income, your focus is survival and stability: reducing fixed costs where possible and increasing income if realistic.

If you have room after essentials, you can start directing money toward stability and growth in a more intentional way.

Step 4: Build a Gentle Spending Plan (Not a Punishing Budget)

Instead of tracking every dollar forever, create a simple structure that protects what matters most.

Use three main categories:

- Must-Haves: essentials you listed earlier.

- Nice-to-Haves: dining out, shopping, subscriptions, travel, beauty, hobbies.

- Future You: savings, investing, extra debt payments.

Decide on rough percentages that feel realistic for the next three months, not forever. For example:

- 60% Must-Haves

- 20% Nice-to-Haves

- 20% Future You

Adjust based on your life. High cost-of-living area? Your Must-Haves might be 70%. Heavy debt season? Future You might temporarily be more about debt payoff than investing.

Then choose one or two places to make small, specific shifts. For example:

- Cap rideshares at a certain amount per month.

- Pause two subscriptions you barely use.

- Move one recurring expense to a cheaper option.

Small changes, repeated, create more breathing room than one dramatic, unsustainable overhaul.

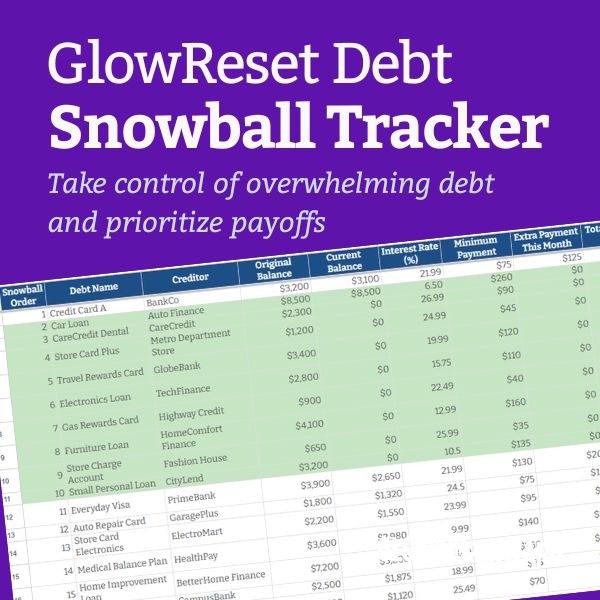

Step 5: Prioritize Debt Without Letting It Run Your Life

If you feel behind, debt is often the loudest voice in your head. You can address it without letting it define you.

From your snapshot, list your debts by interest rate. Highlight anything above 6–7% interest. These are usually your priority after you cover essentials and a small emergency buffer.

Choose one primary strategy:

- Highest interest first (avalanche): mathematically efficient, saves the most money over time.

- Smallest balance first (snowball): emotionally motivating, gives quick wins.

There is no wrong choice. Pick the one you are most likely to stick with. Commit to paying the minimum on all debts, then send any extra you can consistently afford to your chosen target debt.

If your debt feels unmanageable even with a plan, consider support: a reputable nonprofit credit counseling agency, a financial therapist, or a fee-only financial planner who understands your values.

Step 6: Protect Future You with Simple Automation

Once your basics are covered, automation helps you move forward even when life is busy.

Consider automating:

- Bill payments for essentials to avoid late fees.

- Transfers to savings for an emergency fund, even if it is a small amount.

- Retirement contributions through your employer or an IRA.

If you are not currently investing, start with what feels doable, not what feels impressive. Even 1–3% of your income is a meaningful start. You can always increase later.

Label your accounts clearly: “Emergency Fund,” “Travel 2025,” “Sabbatical,” “Down Payment,” or anything that reflects your real goals. Names make the money feel more purposeful and less abstract.

Step 7: Create a Monthly Money Check-In Ritual

Instead of avoiding your accounts until there is a crisis, build a calm, 20–30 minute ritual once a month.

Make it as pleasant as possible:

- Choose a time when you are not rushed.

- Make tea or coffee, light a candle, play music.

- Use the same notebook or digital document each month.

During your check-in, review:

- Current balances in bank, debt, and investment accounts.

- Any big expenses coming up in the next 30–60 days.

- Whether your Must-Haves, Nice-to-Haves, and Future You percentages still feel right.

Ask yourself:

- What worked with money this month?

- What felt stressful?

- What is one small adjustment I can make next month?

This is about staying in relationship with your money, not controlling every detail.

Step 8: Release the Timeline Pressure

Feeling behind often comes from comparing your path to someone else’s highlight reel or to an outdated script about what you “should” have by a certain age.

Remind yourself:

- Careers are not linear anymore.

- Many people rebuild financially after divorce, illness, career changes, or supporting family.

- Your worth is not measured by net worth, home ownership, or investment balances.

Your job is not to catch up to an invisible standard. Your job is to care for the current and future versions of you with the information and resources you have right now.

Choose one next step from this guide and schedule it in your calendar within the next week. That might be creating your money snapshot, setting up one automatic transfer, or planning your first monthly check-in.

You do not have to fix everything at once. You only have to keep moving, gently, in the direction of clarity and support.