Feeling Behind With Money? A Calm, Clear Way To Catch Up

You can be successful on paper and still feel behind with money.

Maybe your career looks impressive, but your savings don’t. Maybe you earn well, yet debt and daily expenses keep you stuck in a loop. Or you’re simply tired of feeling like you “should” be further ahead by now.

This isn’t a character flaw. It’s a signal: your money life needs structure that actually fits you, not more pressure or perfection.

Step 1: Pause the self-judgment so you can see clearly

When you feel behind, it’s easy to jump into extreme fixes: strict budgets, intense side hustles, or complicated investing strategies. But if your nervous system is already overloaded, those plans rarely last.

Before any numbers, give yourself a mental reset:

- Separate your worth from your net worth. Your balance sheet is data, not a verdict on your value, intelligence, or potential.

- Drop the comparison game. You see other people’s highlight reels, not their credit card statements, family help, or financial anxiety.

- Shift from “I’m behind” to “I’m getting current.” Language matters. You’re not fixing a failure; you’re updating a system.

This mindset shift doesn’t solve everything, but it gives you enough emotional space to make decisions that are calm, not panicked.

Step 2: Get your true financial snapshot in 30–45 minutes

You don’t need a full spreadsheet empire to start. You just need a clear snapshot of where you are today.

Set a timer for 30–45 minutes and write down:

- Income (monthly, after tax): salary, bonuses (averaged), side income.

- Fixed essentials: rent or mortgage, utilities, groceries, transportation, insurance, childcare, minimum debt payments.

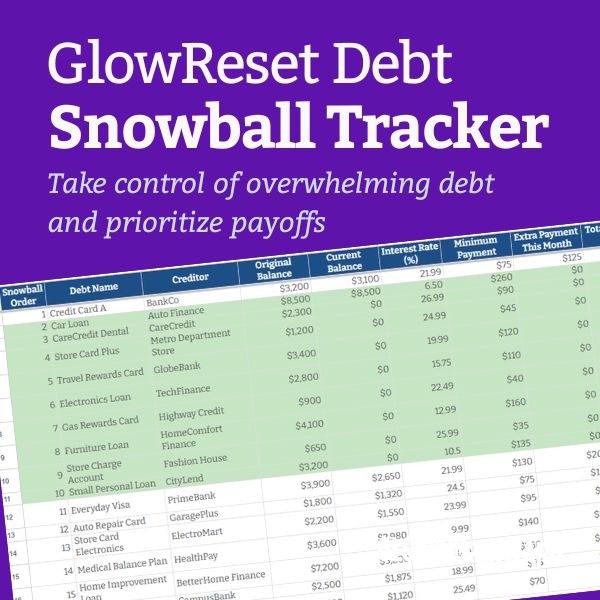

- Debts: balances, interest rates, and minimum payments for each card or loan.

- Cash and savings: checking, savings, emergency fund, short-term sinking funds.

- Investments: retirement accounts, brokerage accounts, employer stock.

Keep it simple. Round to the nearest $10 or $100. The goal is clarity, not precision to the penny.

If this feels emotionally heavy, break it into two sessions: one for income and expenses, one for debts and savings. You’re allowed to go at a sustainable pace.

Step 3: Define what “caught up” actually means for you

Feeling behind is vague. Your brain needs something more specific than “I should have more money by now.”

Translate “caught up” into 2–3 concrete targets for the next 12–24 months. For example:

- “Have a 3‑month emergency fund so I can breathe.”

- “Pay off my highest-interest credit card and stop adding new debt.”

- “Consistently invest 10% of my income for future me.”

Notice these are not about matching someone else’s lifestyle. They’re about stability, options, and relief.

Once you have your targets, rank them:

- Priority 1: What would reduce your stress the most?

- Priority 2: What protects your future self?

- Priority 3: What improves daily life in a realistic way?

Clarity turns vague anxiety into a direction.

Step 4: Build a “good enough” monthly money plan

Instead of a strict budget you’ll abandon in three weeks, create a simple, flexible plan you can actually live with.

Start with your monthly take-home income and assign it in this order:

- 1. Essentials: housing, food, transportation, childcare, insurance, minimum debt payments.

- 2. Safety and stability: emergency fund, small buffer in checking, any past-due bills.

- 3. High-impact goals: extra debt payments, retirement contributions, short-term savings (e.g., car repairs, travel, moving).

- 4. Guilt-free spending: dining out, beauty, clothes, experiences, convenience support (cleaning, childcare help, etc.).

If your numbers don’t fit, adjust in this order:

- Trim or pause lower-priority spending before touching essentials.

- Look for “leaks” (subscriptions, fees, impulse buys) rather than cutting every joy.

- Consider small income boosts that don’t burn you out: a targeted freelance project, asking for a raise, or renegotiating your role.

Your plan is “good enough” if you can name where your money is going, you’re covering essentials, and at least one small step is happening toward your top priority.

Step 5: Create one simple system for each money area

To move from overwhelm to progress, think in systems, not willpower. For each area, choose one simple system:

- Bills: Put fixed bills on auto-pay where possible. For the rest, choose one “money day” per month to pay and review.

- Savings: Automate a small transfer each payday, even if it’s $25. You can increase later.

- Debt: Pick a focus debt (usually the highest interest) and set a fixed extra payment amount. Automate it if you can.

- Spending: Use one main card or account for daily spending so you can see patterns clearly.

Systems reduce decision fatigue. You don’t need to think about money all day; you just need a few intentional moments each month.

Step 6: Protect your emotional bandwidth

Money stress is rarely just about math. It’s also about exhaustion, expectations, and invisible labor.

To protect your energy while you improve your finances:

- Set a “worry window.” Give yourself 15–20 minutes, once or twice a week, to look at accounts, make decisions, and write down next steps. Outside that window, when worry pops up, remind yourself, “I have time scheduled for this.”

- Use neutral language. Replace “I’m terrible with money” with “I’m learning new skills” or “I’m updating my systems.”

- Ask for support. This might be a financial planner, a money coach, a therapist, or a trusted friend who can be a calm sounding board.

Emotional regulation is a financial skill. When you’re less flooded, you make better decisions and stick to your plan more easily.

Step 7: Choose your “minimums” for hard weeks

Life will get busy. Work will spike. Family needs will expand. Those are the weeks when old patterns try to come back.

Instead of expecting yourself to keep up a perfect routine, define your money “minimums” for hard weeks:

- Check accounts once.

- Let your automations run.

- Pause non-essential extra payments if needed, without shame.

- Spend 5 minutes confirming you’re still on track with your top priority.

Minimums keep you connected to your plan without demanding full capacity. This is how progress becomes sustainable instead of all-or-nothing.

Step 8: Measure progress by behavior, not just balances

Balances grow slowly at first, especially if you’re starting with debt or limited savings. If you only measure success by big numbers, you’ll feel like nothing is happening.

Track progress by behavior:

- Did you follow your money day this month?

- Did your emergency fund grow, even by $20?

- Did your total debt balance move down, even slightly?

- Did you avoid adding new debt this week?

These are real wins. They compound over time, even when they don’t feel dramatic.

What “caught up” can feel like

Being financially “caught up” doesn’t mean having everything perfect or never worrying again. It often looks like:

- Knowing your numbers without dread.

- Having a small but real cushion for surprises.

- Seeing debt balances move in the right direction.

- Investing something for your future, even if it’s not as much as you’d like yet.

- Trusting yourself to make money decisions without spiraling.

You don’t need a different personality, a different job, or a different past to get there. You need clarity, a few simple systems, and a plan that respects your real life.

You’re not behind. You’re right on time to build the version of your financial life that actually supports you.