Feeling Behind Financially: A Calm, Clear Reset for Your Money Life

You can be smart, accomplished, and still feel behind with money.

Maybe your income looks good, but your savings don’t. Maybe debt feels heavy, or you’re tired of pretending you “have it together” financially when it feels chaotic inside.

This isn’t a character flaw. It’s a system problem. And systems can be redesigned.

Let’s walk through a calm, step-by-step reset so your money life starts to feel clear, doable, and aligned with the woman you actually are.

Step 1: Separate your self-worth from your net worth

Before any numbers, you need one boundary: your value as a person is not up for debate.

Money is data. Not a verdict.

If you notice thoughts like “I’m bad with money” or “I should be further along by now,” pause and reframe:

- Old story: “I’m irresponsible.”

New story: “No one taught me this, and I’m learning now.” - Old story: “It’s too late.”

New story: “Today is the earliest I can start from where I am.”

This shift matters. When money becomes neutral information instead of a judgment, you can look at it clearly and make better decisions.

Step 2: Do a 20-minute money snapshot (not a full audit)

You don’t need a color-coded spreadsheet to get started. You just need a snapshot.

Set a 20-minute timer. On one page, write three lists:

- 1. Cash & savings: checking, savings, emergency fund, any cash-like accounts.

- 2. Debt: credit cards, student loans, personal loans, car loans, any “buy now, pay later.”

- 3. Monthly must-pays: rent/mortgage, utilities, minimum debt payments, insurance, childcare, subscriptions you actually use.

Don’t dig for every tiny detail. If you’re unsure, estimate. The goal is visibility, not perfection.

When the timer ends, stop. You can come back another day. This keeps the process from feeling like a marathon you never want to repeat.

Step 3: Define what “secure enough” looks like for you

Many women feel behind because they’re chasing a vague idea of “being set.” There’s no finish line, so it never feels like enough.

Instead, define your version of “secure enough.” Not your parents’ version. Not social media’s version. Yours.

Consider these questions:

- How much would you like in an emergency fund to feel steady? (Often 3–6 months of must-have expenses.)

- What level of debt payoff would make you breathe easier in the next 12–24 months?

- What would “basic future you support” look like? (For example, consistently contributing to retirement, even if it’s a small amount.)

Turn this into a simple statement, like:

- “Secure enough for me = 4 months of expenses saved, no credit card balances, and at least $300/month going to retirement.”

Now you have a direction. You’re not chasing a feeling; you’re moving toward a definition.

Step 4: Build a calm, realistic spending plan

Think of a spending plan as a values map, not a punishment. It tells your money where to go so you’re not wondering where it went.

Start with three categories:

- Essentials: housing, utilities, groceries, transportation, minimum debt payments, childcare, insurance.

- Future you: savings, investing, extra debt payments.

- Enjoyment: dining out, travel, beauty, hobbies, gifts, convenience purchases.

Look at your income after taxes. Assign rough percentages:

- Essentials: often 50–60%

- Future you: aim for 10–25% (start where you are)

- Enjoyment: whatever remains

If the numbers don’t work, adjust, not judge. Maybe essentials are high right now. Maybe “future you” starts at 5%. That’s still progress.

The goal is to create a plan you can actually live with, not a fantasy that collapses in two weeks.

Step 5: Choose one “money lever” to move this month

When you feel behind, it’s tempting to try to fix everything at once. That usually leads to burnout and avoidance.

Instead, pick one lever for the next 30 days:

- Income lever: Ask for a raise, adjust your rates, take on one intentional side project, or finally bill for work that’s overdue.

- Spending lever: Pause or downgrade 2–3 subscriptions, set a weekly dining-out limit, or create a simple grocery plan.

- Debt lever: Choose one card or loan to focus on and add a specific extra amount this month, even if it’s small.

- Savings lever: Automate a transfer on payday, even if it’s $25. Automation beats willpower.

One lever, clearly defined, is more powerful than ten vague intentions.

Step 6: Create a 15-minute weekly money ritual

Consistency matters more than intensity.

Choose one day and time you can usually protect—Sunday evening, Friday lunch, or Monday morning. Set a 15-minute recurring calendar event called “Money Check-In.”

During that time, you simply:

- Open your accounts (no bracing, just observing).

- Note your balances and any upcoming bills.

- Move money according to your plan (pay a bill, transfer to savings, make an extra debt payment).

- Ask: “Is there anything this week that needs a small adjustment?”

That’s it. No full rework. No perfection. Just staying in relationship with your money instead of avoiding it.

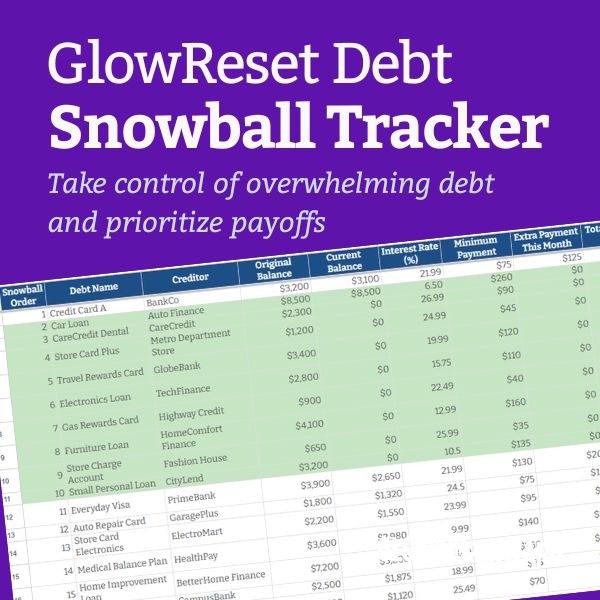

Step 7: Make debt a project, not a personality

Debt can feel like a secret shame. It doesn’t need to.

Debt is a tool you used at a certain point in your life. Now you’re deciding how and when to put it down.

Turn it into a project:

- List each debt with balance, interest rate, and minimum payment.

- Decide on a strategy: highest interest first (saves money) or smallest balance first (builds momentum).

- Choose a realistic extra amount you can send each month toward your focus debt.

Track progress in a simple way: a note on your phone, a sticky note on your desk, or a simple chart. Watching balances drop—even slowly—can be surprisingly grounding.

Step 8: Support your nervous system, not just your bank account

Money stress is not just about math. It’s about your nervous system.

If you notice anxiety spike when you deal with money, try pairing money tasks with regulation:

- Light a candle or make tea before your money check-in.

- Take three slow breaths before opening your banking app.

- Set a timer so you know there’s an end point.

- Play calm music or a favorite playlist while you review numbers.

The goal is to teach your body: “We can look at money and still feel safe.” Over time, this makes everything easier.

Step 9: Decide what “wealth” actually means to you

It’s easy to absorb someone else’s definition of wealth: a certain house, a certain car, a certain lifestyle.

But real financial peace comes from aligning money with what you actually care about.

Ask yourself:

- What do I want more of in my life that money can support? (Time, freedom, experiences, stability, generosity?)

- What am I willing to spend less on so I can have more of what matters?

- If my money fully reflected my values, what would change over the next year?

Let your answers guide your choices more than comparison or pressure.

Step 10: Give yourself permission to be “in progress”

You are allowed to be successful and still learning about money.

You are allowed to have made choices that no longer fit who you are now.

You are allowed to start over as many times as you need.

Feeling behind doesn’t mean you are behind. It usually means you haven’t had a clear, compassionate plan that fits your real life.

Today can be the day you shift from “I should have figured this out by now” to “I’m figuring this out now.”

That’s powerful. And it’s more than enough.