Debt Free in 90 Days: The Ultimate Money Challenge

Let’s be honest—carrying debt can feel like dragging a backpack full of bricks uphill. Whether it’s credit cards, student debt, or personal loans, those balances don’t just weigh on your wallet—they weigh on your peace of mind. But what if I told you it’s possible to make serious progress—or even become completely debt-free—in just 90 days? That’s right. With the right strategy, mindset, and consistent action, you can transform your financial future starting today.

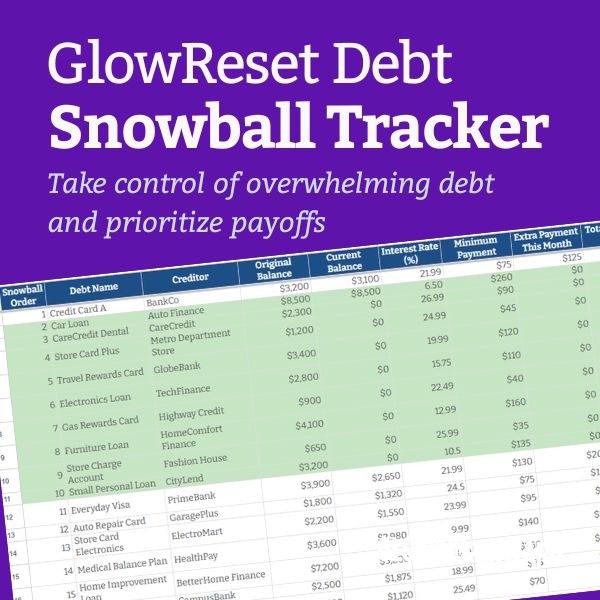

Step 1: Face the Numbers

Before you can crush your debt, you need a clear picture of what you’re dealing with. Grab a notebook, spreadsheet, or budgeting app and write down every debt you owe:

Credit cards (list each card, balance, interest rate, and minimum payment)

Student debt (include loan servicer, balance, and monthly payment)

Personal or auto loans

Any other outstanding debts

Total it up. This number might feel overwhelming, but don’t let it scare you. Knowledge is power, and now you’re in control.

Step 2: Pick Your Payoff Strategy

There are two popular methods to tackle debt: the debt snowball and the debt avalanche. Choose the one that matches your motivation style:

Debt Snowball: Pay off the smallest debt first, while making minimum payments on the rest. This gives you quick wins and builds momentum.

Debt Avalanche: Pay off the debt with the highest interest rate first. This saves you the most money in the long run.

Either strategy works—as long as you stick with it. If motivation is your fuel, snowball might be best. If saving money is your priority, avalanche is the way to go.

Step 3: Build a 90-Day Budget That Works

Now it’s time to zero in on your spending. For the next 90 days, every dollar should serve your debt payoff goal. Start by tracking your spending from the past month. Identify non-essential expenses like:

Streaming services you barely use

Takeout meals and daily coffee runs

Subscription boxes or unused memberships

Cut or pause anything that isn’t necessary. Then, reallocate those dollars toward your debt. Even $100 a month in savings adds up to $300 in 90 days—money that could knock out a credit card balance or make a big dent in a loan.

Pro Tip: Automate Your Payments

Set up automatic payments for your minimums plus any extra you can afford. This removes the temptation to spend that money elsewhere and ensures you stay on track.

Step 4: Increase Your Income

If cutting costs isn’t enough to meet your 90-day goal, it’s time to boost your income. Here are some quick ways to bring in extra cash:

Freelance or consult: Use your skills in writing, design, tutoring, or marketing.

Sell unused items: Declutter your home and list clothes, gadgets, or furniture online.

Take a side gig: Drive for a delivery app, babysit, or offer handyman services.

Cash-back apps: Use apps that reward you for everyday shopping.

Every extra dollar should go directly toward your debt. Think of it as buying your freedom.

Step 5: Stay Focused and Motivated

Paying off debt quickly takes discipline, but that doesn’t mean it has to be miserable. Keep yourself motivated by:

Tracking your progress visually: Create a debt thermometer or a checklist you can update weekly.

Celebrating small wins: Every time you pay off a balance, do something low-cost and fun—like a movie night at home or a celebratory walk in the park.

Joining a challenge: Invite a friend to do the 90-day challenge with you or find an online community to share wins and support.

What Happens After 90 Days?

Even if you don’t pay off all your debt in 90 days, the habits and momentum you build are priceless. You’ll be more confident managing money, more intentional with your spending, and more motivated to reach long-term financial goals—like saving for a home, investing, or finally going on that dream vacation.

And if you do hit your goal? Celebrate big (without falling back into debt) and start planning your next money move. Whether it’s building an emergency fund or investing for the future, you’re in control now.

Let’s Recap Your 90-Day Debt Payoff Plan

List all your debts and know your numbers

Choose a payoff strategy: snowball or avalanche

Cut expenses and create a focused budget

Find ways to earn extra income

Track progress and stay motivated

You’ve got the plan. You’ve got the tools. Now you’ve just got to take the first step. In 90 days, your future self will thank you—and your bank account will too.

Debt doesn’t have to be forever. With strategy, commitment, and a little hustle, you can break free from credit cards, student debt, and loans—and start building wealth instead. Ready to rise above it all? Let’s go.